Microsoft Corp. plans to hire "several thousand" new employees in China to work on its Azure cloud computing system and smartphones using its Windows operating system, CEO Steve Ballmer said. Bloomberg reports the new hires will be added to an existing Chinese workforce of 4,000, and Ballmer said China has become the fastest growing market for Microsoft’s (NASDAQ: MSFT) smartphone operating system.

Reported by bizjournals 1 hour ago.

↧

Microsoft to hire 'several thousand' in China, says Ballmer

↧

Over 75 million smartphones sold in China during Q1

It’s a good time to sell smartphones in China. According to stats compiled from DigiTimes, 90.54 million mobile phones were sold in China during the first quarter of 2013, for a gain of 23.5%. Year-over-year the gain was 34%.

It’s a good time to sell smartphones in China. According to stats compiled from DigiTimes, 90.54 million mobile phones were sold in China during the first quarter of 2013, for a gain of 23.5%. Year-over-year the gain was 34%.[ Continue reading...]

The post Over 75 million smartphones sold in China during Q1 appeared first on Geeky Gadgets. Reported by Geeky Gadgets 1 hour ago.

↧

↧

New CCTV Cameras Waterproof CCTV Video Security Camera Released From China

Ankaka Releases New CCTV Cameras Waterproof CCTV Video Security Camera with Adjustable Focus and Night vision.

CCTV Cameras

Ankaka Releases New CCTV Cameras Waterproof CCTV Video Security Camera with Adjustable Focus and Night vision.Anyone who cares about security will appreciate this durable CCTV camera. This super security camera with sony super HAD CCD is easy to mount and install. It is equipped with 4-9 mm Manual Zoom Lens and a clear 540 TVL resolution which provides high quality images. The viewing distance ranges from 80 to 100 meters during the daytime and approximately 50 meters during nighttime with 42 infrared LEDs. The CCTV cameras operate in the 10 to 50 C temperature range. The shutter speed varies from a relatively slow 1/50 rate to a rapid 1/100,000 second rate.Additional features include a respectable signal-to-noise ratio greater than 48 db, automatic white balance, and a two to one interlace scanning system.

This new Super Security Camera gives people all the performance people would expect from famous brand videocamera, but gives people a factory-direct wholesale price. With increased security and complete peace in mind, the D21019 is proudly brought to people by - Ankaka

Item specifics From The Factory:

Lens: 4-9 mm manual zoom lens

Color System: PAL / NTSC

Horizontal Resolution: 540 TV Lines

Scanning System: 2:1 Interlace

Shutter Speed: 1/50 (1/60) ~ 1/100,000 sec

IR: 42 LEDs for infrared night vision

Viewing Distance:

- Daytime: 80 - 100 meters

- Nighttime (IR): 50 meters

White Balance: Auto

S/N Ratio: > 48 db (ACG OFF)

Video Output: 1.0Vp-p.75 ohm

Power Adapter: DC12V, 350mA

Working Temperature: - 10 ~ 50 degree C

Dimensions: 145 x 75 x 95 mm

Primary Function: CCTV Video Security Camera

Image Sensor: 1/3 Inch SONY Super HAD CCD

Minimum Illumination: 0 LUX (IR ON)

Effective Pixels: PAL:512 (H) x 582 (V) / NTSC: 512(H) x 492 (V)

This CCTV Cameras Key Functions:

4-9 mm Manual Zoom Lens

1/3 Sony Super HAD CCD

Waterproof CCTV Video Security Camera

Easy to Mount annd Install

42 IR LEDs for 50m Night Vision Range

China wholesale security cameras are offered online here at this resource:http://www.ankaka.com/Wholesale-security-cameras_c10089

About Ankaka.com

Ankaka.com is an online wholesale electronics retailer that has partnered with more than 400 firms in China to ship consumer electronics at discounted prices throughout the globe, ensuring the best deals on the Internet.The company has been providing unmatched deals on consumer electronics since 2005, and its online store is packed with a range of thousands of varying products, which is why Ankaka fans consider it to be ideal retailers to dropship electronics from China.

Contact Information:

Contact Person: Jun Chen

Company Name: Ankaka Limited

Call: 01186-755-82771810

Contact Email: sale@ankaka.com

Address: 313, Building 201, Shangbu Industrial Park, Huaqiangbei Road, Futian District, Shenzhen, China

postal code: 518100

Company Contact Information

Ankaka Limited

Ankaka

shenzhen,huaqiangbei

518000

0118675582771810

News and Press Release Distribution From I-Newswire.com Reported by i-Newswire.com 1 hour ago.

CCTV Cameras

Ankaka Releases New CCTV Cameras Waterproof CCTV Video Security Camera with Adjustable Focus and Night vision.Anyone who cares about security will appreciate this durable CCTV camera. This super security camera with sony super HAD CCD is easy to mount and install. It is equipped with 4-9 mm Manual Zoom Lens and a clear 540 TVL resolution which provides high quality images. The viewing distance ranges from 80 to 100 meters during the daytime and approximately 50 meters during nighttime with 42 infrared LEDs. The CCTV cameras operate in the 10 to 50 C temperature range. The shutter speed varies from a relatively slow 1/50 rate to a rapid 1/100,000 second rate.Additional features include a respectable signal-to-noise ratio greater than 48 db, automatic white balance, and a two to one interlace scanning system.

This new Super Security Camera gives people all the performance people would expect from famous brand videocamera, but gives people a factory-direct wholesale price. With increased security and complete peace in mind, the D21019 is proudly brought to people by - Ankaka

Item specifics From The Factory:

Lens: 4-9 mm manual zoom lens

Color System: PAL / NTSC

Horizontal Resolution: 540 TV Lines

Scanning System: 2:1 Interlace

Shutter Speed: 1/50 (1/60) ~ 1/100,000 sec

IR: 42 LEDs for infrared night vision

Viewing Distance:

- Daytime: 80 - 100 meters

- Nighttime (IR): 50 meters

White Balance: Auto

S/N Ratio: > 48 db (ACG OFF)

Video Output: 1.0Vp-p.75 ohm

Power Adapter: DC12V, 350mA

Working Temperature: - 10 ~ 50 degree C

Dimensions: 145 x 75 x 95 mm

Primary Function: CCTV Video Security Camera

Image Sensor: 1/3 Inch SONY Super HAD CCD

Minimum Illumination: 0 LUX (IR ON)

Effective Pixels: PAL:512 (H) x 582 (V) / NTSC: 512(H) x 492 (V)

This CCTV Cameras Key Functions:

4-9 mm Manual Zoom Lens

1/3 Sony Super HAD CCD

Waterproof CCTV Video Security Camera

Easy to Mount annd Install

42 IR LEDs for 50m Night Vision Range

China wholesale security cameras are offered online here at this resource:http://www.ankaka.com/Wholesale-security-cameras_c10089

About Ankaka.com

Ankaka.com is an online wholesale electronics retailer that has partnered with more than 400 firms in China to ship consumer electronics at discounted prices throughout the globe, ensuring the best deals on the Internet.The company has been providing unmatched deals on consumer electronics since 2005, and its online store is packed with a range of thousands of varying products, which is why Ankaka fans consider it to be ideal retailers to dropship electronics from China.

Contact Information:

Contact Person: Jun Chen

Company Name: Ankaka Limited

Call: 01186-755-82771810

Contact Email: sale@ankaka.com

Address: 313, Building 201, Shangbu Industrial Park, Huaqiangbei Road, Futian District, Shenzhen, China

postal code: 518100

Company Contact Information

Ankaka Limited

Ankaka

shenzhen,huaqiangbei

518000

0118675582771810

News and Press Release Distribution From I-Newswire.com Reported by i-Newswire.com 1 hour ago.

↧

Pope Francis urges China's Catholics to stay loyal to Rome

ROME (Reuters) - Pope Francis on Wednesday urged Catholics in China to remain loyal to the Vatican, whose authority is challenged by China's Communist rulers.

Reported by Reuters India 13 minutes ago.

↧

Golf Clap for China Distance Education Holdings

Filed under: Investing

Filed under: Investing*China Distance Education Holdings* (NYS: DL) reported earnings on May 21. Here are the numbers you need to know.

*The 10-second takeaway

* For the quarter ended March 31 (Q2), China Distance Education Holdings met expectations on revenues and met expectations on earnings per share.

Compared to the prior-year quarter, revenue grew. GAAP earnings per share dropped significantly.

Margins shrank across the board.

*Revenue details

* China Distance Education Holdings recorded revenue of $13.0 million. The two analysts polled by S&P Capital IQ expected revenue of $13.1 million on the same basis. GAAP reported sales were 5.4% higher than the prior-year quarter's $12.3 million.

Source: S&P Capital IQ. Quarterly periods. Dollar amounts in millions. Non-GAAP figures may vary to maintain comparability with estimates.

*EPS details

* EPS came in at $0.02. The two earnings estimates compiled by S&P Capital IQ predicted $0.02 per share. GAAP EPS of $0.02 for Q2 were 75% lower than the prior-year quarter's $0.08 per share.

Source: S&P Capital IQ. Quarterly periods. Non-GAAP figures may vary to maintain comparability with estimates.

*Margin details

* For the quarter, gross margin was 46.6%, much worse than the prior-year quarter. Operating margin was 5.4%, much worse than the prior-year quarter. Net margin was 6.1%, much worse than the prior-year quarter. (Margins calculated in GAAP terms.)

*Looking ahead

* Next quarter's average estimate for revenue is $16.5 million. On the bottom line, the average EPS estimate is $0.09.

Next year's average estimate for revenue is $65.5 million. The average EPS estimate is $0.34.

*Investor sentiment*

Of Wall Street recommendations tracked by S&P Capital IQ, the average opinion on China Distance Education Holdings is outperform, with an average price target of $7.00.

Can your portfolio provide you with enough income to last through retirement? You'll need more than China Distance Education Holdings. Learn how to maximize your investment income and "Secure Your Future With 9 Rock-Solid Dividend Stocks." Click here for instant access to this free report.

· Add China Distance Education Holdings to My Watchlist.

The article Golf Clap for China Distance Education Holdings Reported by DailyFinance 50 minutes ago.

↧

↧

China's Premier Seeks Stronger Ties with Pakistan

China's prime minister has arrived in Pakistan where he is seeking to strengthen cooperative ties between the two countries. Trade between China and Pakistan hit $12 billion last year and both sides want to raise that to $15 billion in the next two to three years.

Reported by VOA News 24 minutes ago.

↧

The Latest Floor Plan for Furniture China 2013

SHANGHAI, May 22, 2013 /PRNewswire/ -- Furniture China 2013 will be held from 11-15 September, 2013. Free Registration now to get your personal admission badge for Furniture China 2013! Via the updated floor plan, occupying all 17 of the existing exhibition halls at...

Reported by PR Newswire 3 minutes ago.

↧

Metal Casket Promotion from China Casket Manufacturer MillionaireCasket.com

Recently, MillionaireCasket.com, a leading casket company from China, has announced a metal casket promotion, and this promotion will be valid till the end of May 2013.

(PRWEB) May 23, 2013

Recently, MillionaireCasket.com, a leading casket company from China, has announced a metal casket promotion, and this promotion will be valid until May 31, 2013.

MillionaireCasket.com has been manufacturing different types of metal caskets for many years. All their caskets come with intricate designs and secure locking systems. As a leading China casket manufacturer, MillionaireCasket.com is well known in the industry for providing high-quality caskets, and the company has become one of the leading casket suppliers in the market.

The promotion of metal caskets is to show appreciation to customers who continuously provide a positive feedback. The comprehensive ISO9001-2000 compliance quality control program allows the company to supply good caskets for customers worldwide.

The caskets come in 16, 18, or 20 gauge metal and the company provides OEM services to customers as well. The interior of these caskets are also damage free; it is treated with chemicals to safeguard it from rusting or corroding. The caskets can be ordered in any desired measurement and weight. Simple ones are also available as well as designed ones.

Moreover, MillionaireCasket.com is also involved in casket wholesale business. Along with caskets, it also offers several other products related to funerals. Hence, it is a one stop funeral supplier.

MillionaireCasket.com is a China based company supplying several different types of caskets and all sorts of funeral material. It is a one stop shop for buying high quality reliable funeral products. Reported by PRWeb 11 hours ago.

(PRWEB) May 23, 2013

Recently, MillionaireCasket.com, a leading casket company from China, has announced a metal casket promotion, and this promotion will be valid until May 31, 2013.

MillionaireCasket.com has been manufacturing different types of metal caskets for many years. All their caskets come with intricate designs and secure locking systems. As a leading China casket manufacturer, MillionaireCasket.com is well known in the industry for providing high-quality caskets, and the company has become one of the leading casket suppliers in the market.

The promotion of metal caskets is to show appreciation to customers who continuously provide a positive feedback. The comprehensive ISO9001-2000 compliance quality control program allows the company to supply good caskets for customers worldwide.

The caskets come in 16, 18, or 20 gauge metal and the company provides OEM services to customers as well. The interior of these caskets are also damage free; it is treated with chemicals to safeguard it from rusting or corroding. The caskets can be ordered in any desired measurement and weight. Simple ones are also available as well as designed ones.

Moreover, MillionaireCasket.com is also involved in casket wholesale business. Along with caskets, it also offers several other products related to funerals. Hence, it is a one stop funeral supplier.

MillionaireCasket.com is a China based company supplying several different types of caskets and all sorts of funeral material. It is a one stop shop for buying high quality reliable funeral products. Reported by PRWeb 11 hours ago.

↧

China Zenix Auto International Schedules 2013 First Quarter Press Release and Conference Call for May 24, 2013

ZHANGZHOU, China, May 23, 2013 /PRNewswire/ -- China Zenix Auto International Limited (NYSE: ZX) ("Zenix Auto" or "the Company"), the largest commercial vehicle wheel manufacturer in China in both...

Reported by FinanzNachrichten.de 11 hours ago.

↧

↧

NKorean Envoy Makes Public Show Of Respect For China

BEIJING -- On a visit to repair ties with China and waiting to meet its leader, a North Korean envoy Thursday paid deference to its chief ally's hopes for renewed multinational nuclear talks.

Choe Ryong Hae, at a meeting with Communist Party official Liu Yunshan, praised China's work on behalf of peace and stability and its "great efforts to return (Korean) peninsular issues to the channel of dialogue and negotiation."

North Korea "is willing to accept the suggestion of the Chinese side and launch dialogue with all relevant parties," Choe was quoted as saying by Chinese state broadcaster CCTV.

While Choe's remarks were vague and offered no hint of hoped-for concessions, they served as a public show of respect after a half-year of rising frustration in Beijing at Pyongyang and its recent rocket and nuclear tests and other saber-rattling.

Diplomatic snubs and this month's seizure of a Chinese fishing crew, who were allegedly held for ransom by a North Korean military unit, have further soured the mood in Beijing and among the Chinese public.

A vice marshal in the North Korean military, Choe was sent to Beijing on Wednesday on a fence-mending visit as a special envoy for North Korean leader Kim Jong Un.

As such, North Korea watchers say he is expected to hold talks with Chinese President Xi Jinping. His comments Thursday will likely be seen by Beijing as setting the correct atmosphere of deference for such a meeting.

Xi was in southwest China's Sichuan province on Thursday overseeing earthquake recovery efforts and it wasn't clear when he planned to return to the capital.

Choe also spent part of Thursday touring an industrial park in the southern part of the Beijing, accompanied by a Communist Party functionary. China has long sought to convince the North to adopt its model of economic reform accompanied by rigid one-party rule. Reported by Huffington Post 10 hours ago.

Choe Ryong Hae, at a meeting with Communist Party official Liu Yunshan, praised China's work on behalf of peace and stability and its "great efforts to return (Korean) peninsular issues to the channel of dialogue and negotiation."

North Korea "is willing to accept the suggestion of the Chinese side and launch dialogue with all relevant parties," Choe was quoted as saying by Chinese state broadcaster CCTV.

While Choe's remarks were vague and offered no hint of hoped-for concessions, they served as a public show of respect after a half-year of rising frustration in Beijing at Pyongyang and its recent rocket and nuclear tests and other saber-rattling.

Diplomatic snubs and this month's seizure of a Chinese fishing crew, who were allegedly held for ransom by a North Korean military unit, have further soured the mood in Beijing and among the Chinese public.

A vice marshal in the North Korean military, Choe was sent to Beijing on Wednesday on a fence-mending visit as a special envoy for North Korean leader Kim Jong Un.

As such, North Korea watchers say he is expected to hold talks with Chinese President Xi Jinping. His comments Thursday will likely be seen by Beijing as setting the correct atmosphere of deference for such a meeting.

Xi was in southwest China's Sichuan province on Thursday overseeing earthquake recovery efforts and it wasn't clear when he planned to return to the capital.

Choe also spent part of Thursday touring an industrial park in the southern part of the Beijing, accompanied by a Communist Party functionary. China has long sought to convince the North to adopt its model of economic reform accompanied by rigid one-party rule. Reported by Huffington Post 10 hours ago.

↧

MQ-C4 Triton Drone Makes First Flight: Navy Will Use It To Keep Tabs On China, North Korea [PHOTOS]

![MQ-C4 Triton Drone Makes First Flight: Navy Will Use It To Keep Tabs On China, North Korea [PHOTOS]](http://e8be54f42fd955e4caa5-ce5f0c7d1862e66e85cfe22a9ff4fd68.r88.cf3.rackcdn.com/1520-MQ-C4-Triton-Drone-Makes-First-Flight-Navy.jpg) The U.S. Navy's long awaited MQ-4 Triton surveillance drone took its first flight yesterday in Palmdale, California.

The U.S. Navy's long awaited MQ-4 Triton surveillance drone took its first flight yesterday in Palmdale, California.*See what the drone offers >*

A Navy press release, delivered yesterday, points out that with 360-degree scanning capability and an Automatic Identification System — meaning it can classify different types of ships by itself — the MQ-C4 will be the main Naval spying drone at sea from 2015 onwards. There will be five operating bases, one of which will keep watch over the South China Sea and that likely includes China and North Korea.

But even without its state-of-the-art sensors and cameras, the aircraft itself is capable. It can fly for 24 hours at twice the altitude of commercial jets, reaching a maximum height of 60,000 feet (11 miles).

Apart from being used for combat-related surveillance missions, the drone could also keep tabs on piracy, human smuggling, fishery violations, and organized crime.

Here's a break-down of the new drone and how it'll give the Navy even more control of the high seas.

-Here's what the U.S. is watching. These are the 5 main operating bases where the MQ-4C fleet will be used, networking with other Navy and Air Force drones — notice the South China Sea region is under watch.-

-The MQ-C4 is designed for persistent maritime surveillance and intelligence-gathering — its makers say the Navy will have "24/7" coverage. The drone can travel 11,450 miles before it needs to be refueled.-

-Along with its 360-degree scanning, it can capture images or full motion video at high resolution.-

See the rest of the story at Business Insider

Please follow Military & Defense on Twitter and Facebook.

Reported by Business Insider 10 hours ago.

↧

We are responsible for easing relations between India and Pakistan, claims China

China has played a positive role in the continuous easing of the relationship between India and Pakistan, said a state-run daily which added, "China has not played balancing strategy, using one country against the other."

Reported by India Today 10 hours ago.

Reported by India Today 10 hours ago.

↧

The Bronze Swan Arrives: Is The End Of Copper Financing China's "Lehman Event"?

In all the hoopla over Japan's stock market crash and China's PMI miss last night, the biggest news of the day was largely ignored: *copper, *and the fact that copper's ubiquitous arbitrage and rehypothecation role in China's economy through the use of Chinese Copper Financing Deals (CCFD)* is coming to an end. *

In all the hoopla over Japan's stock market crash and China's PMI miss last night, the biggest news of the day was largely ignored: *copper, *and the fact that copper's ubiquitous arbitrage and rehypothecation role in China's economy through the use of Chinese Copper Financing Deals (CCFD)* is coming to an end. *Copper, as China pundits may know, is the key shadow interest rate arbitrage tool, through the use of financing deals that use commodities with high value-to-density ratios such as gold, copper, nickel, which in turn are used as collateral against which USD-denominated China-domestic Letters of Credit are pleged, in what can often result in *a seemingly infinite rehypothecation loop *(see explanation below) between related onshore and offshore entities, allowing loop participants to pick up virtually risk-free arbitrage (i.e., profits), which however boosts China's FX lending and leads to upward pressure on the CNY.

Since the end result of this arbitrage hits China's current account directly, and is the reason for the recent aberrations in Chinese export data that have made a mockery of China's economic data reporting, *China's State Administration on Foreign Exchange (SAFE) on May 5 finally passed new regulations which will effectively end such financing deals. *

The impact of this development can not be overstated: according to independent observers, as well as firms like Goldman, this will not only impact the copper market (very adversely) as copper will suddenly go from a positive return/carry asset to a negative carry asset leading to wholesale dumping from bonded warehouses, but will likely take out a substantial chunk of synthetic shadow leverage out of the Chinese market and economy.

Naturally, for an economy in which credit creation is of utmost importance, the loss of one such key financing channel will have very unintended consequences at best, and could potentially lead to a significant "credit event" in the world's fastest growing large economy at worst.

But before we get into the nuts and bolts of how such CCF deals operate, and what this means for systemic leverage, we bring you this friendly note released by Goldman's Roger Yuan overnight, in which Goldman not only quietly cut their long Copper trading recommendation established on March 1 (at a substantial loss), but implicitly went short the metal with a 12 month horizon: a huge shift for a bank that has been, on the surface, calling for a global renaissance in the global economy, and in which Dr. Copper is a very leading indicator of overall economic health and end demand.

From Goldman:

*Closing: Long LME copper September 2013 contract at $7,482/t, a $236/t (3.1%) loss*

Following the initial sell-off in copper prices in the second half of February 2013, we established a long copper position at $7,718/t in the September contract (on March 1, 2013). We believed that the fall in copper prices, reflecting in part concerns about Chinese activity, was overdone. We reiterated this view on April 22, post further substantial price declines. Since then, prices have rebounded strongly, with the September contract closing at $7,482/t on May 22, up by 10% from the May 1 low of $6,808/t.

*The emergence of the risk that CCFDs unwind over the next 3 months – we had assumed that deals would continue indefinitely – has complicated our near-term bullish copper view (from current prices*). On the one hand, our fundamental short-term thesis is playing out – copper inventories are drawing, copper’s main end-use markets in China are growing solidly (property sales +39% yoy, completions +7% yoy, auto’s output +14% yoy Jan-April 2013), seasonal factors are currently supportive, Chinese scrap availability is tight, positioning also remains short, and policy risks are, arguably, mildly skewed to the upside.

Set against this is the likely near-term unwind in CCFDs and, critically, our view that copper is headed into surplus in 2014 (the window for higher copper prices is shortening). *On net, we now see the risks to our 6-mo forecast of $8,000/t as skewed to the downside, and, in this context, we unwind our September long copper position at $7,482/t, a $236/t (3.1%) loss, given the recent strong rally in LME prices to near our 3-mo target of $7,500/t. *Additionally, *we believe that a further rally in copper prices in the near term would be a good selling opportunity taking a 12-month view** [**ZH: translated: short it].*

*Consumers: *We believe that consumers will have a better opportunity to enter the copper market to buy taking a 12-month view. Following the recent sharp sell-off in zinc we are increasingly bullish on the outlook from current prices and as such believe consumers should take advantage of current low levels.

*Producers: *Our base case of a sharp slowdown in growth of Chinese construction completions in 2014, in the context of above-trend supply growth, presents significant longer-term downside risks to global copper demand growth and prices. Therefore we continue to believe that any further rallies in the copper price in 2013 represent a good opportunity to hedge, and in our view other non-producer market participants should continue to monitor any copper positions in light of the 2014 downside risks.

So just what is the significance of CCFDs? As it turns out, it is huge. Goldman explains (get a cup of coffee first: this is now a simple walk-thru):

The combination of Chinese capital controls and a significant positive domestic (CNY) to foreign (USD) interest rate differential has, in recent years, resulted in the development and implementation of large scale ‘financing deals’ which legally arbitrage the interest rate differential via China’s current account. These Chinese ‘financing deals’ typically use commodities with high value-to-density ratios such as gold, copper, nickel and ‘high-tech’ goods, as a tool to enable interest rate arbitrage. With the notional value of the deals far exceeding the export/import value of the commodities used, and likely significantly contributing to the recent run-up in China’s short-term FX lending (and related upward pressure on the CNY), China’s State Administration of Foreign Exchange (SAFE) announced new regulations to address these issues (May 5), to be implemented in June.

*SAFE’s new policies are, in our view, likely to bring these Chinese ‘financing deals’ to an end over the next 1-3 months*. Having said this, some uncertainty remains around the implementation of the new policies by SAFE and Chinese banks, the speed at which the policies impact the market, and the possibility that new financing deals are “invented”. Owing to these uncertainties, a complete unwind of CCFDs is still at this point considered a risk.

In this note we provide a full example of a typical deal and discuss our understanding of the impact of an unwind in Chinese Copper Financing Deals (CCFDs) 1 on the copper market.

*Our view is that the bulk of copper stored in bonded warehouses in China – at least 510,000t at present, as well as some inbound copper shipments into China – is being used to unlock the CNY-USD interest rate differential*. This material has not been entirely unavailable to the market (deals can be broken if costs rise, such as a tightening of LME spreads), *but the inventory has been effectively financed by factors exogenous to the copper market for some time.*

We find that *a complete unwind of CCFDs would be bearish for copper prices as the copper used to unlock the differential would shift from being a positive return/carry asset to a negative carry asset for those who currently hold it*. As such this inventory will likely become more ‘available’ to the global market. Initially stocks would likely move into the Chinese domestic market to ease the current tightness, until the current SHFE price premium to LME closes.

After the SHFE-LME price arbitrage closes sufficiently, *the remaining bonded stock (over and above day-to-day working flows) would likely shift from bonded warehouses to the LME*. We expect that the ex-China (LME) market would likely see inventory increases as a result, as China draws on bonded stocks instead of importing and as excess bonded stocks are shifted back on to the LME. *We estimate that the ex-China market will need to ‘carry’ a minimum of 200-250kt of additional physical copper over the coming months, equivalent to 4%-5% of quarterly global supply. The latter would most likely result in a widening contango, including downward pressure on cash prices.*

Specifically, the current LME 3-15 month contango is 1.1%, compared to full carry of c.3%-3.5%.

The emergence of this bearish risk – we had assumed that deals would continue indefinitely – complicates our near-term bullish copper view. Indeed, our fundamental short-term thesis is unfolding – copper inventories are drawing, copper’s main end-use markets in China are growing solidly (property sales +39% yoy, completions +7% yoy, auto’s output +14% yoy over the Jan-April 2013 period), seasonal factors are currently supportive, and scrap availability in China is reportedly tight. Positioning also remains short, and policy risks may be mildly skewed to the upside (ECB meeting June 6 and FOMC meeting June 18-19).

The other factors that have recently supported a rebound in copper prices have been mine supply disruptions at Grasberg in Indonesia (c.480kt for 2013E), and the threat of further strikes in Chile ahead of the Chilean elections and at Grasberg ahead of contract negotiations (the current labour contract ends in September). Our forecast 2013 disruption allowance of 5.8%, or c.900kt is designed to account for these kinds of developments, and so far this year our allowance looks reasonable, meaning that these disruptions are not set to impact our overall balance forecast.

Set against this is the likely near-term unwind in CCFDs and, critically, our view that copper is headed into significant surplus in 2014 (the window for higher prices is shortening). On net, we now see the risks to our 6-mo forecast of $8,000/t as skewed to the downside. In this context, we unwind our September long copper recommendation at $7,482/t, a 3% loss.

If you haven't shorted copper after reading the above.... we suggest you re-read it.

Ploughing on: below is the reason for SAFE's new dramatic regulations, and why China decided to go ahead and kill CCFD, unintended consequences be damned:

China’s foreign currency reserves have risen significantly since the start of the year, placing upward pressure on the CNY (Exhibit 1). This development prompted SAFE, China’s regulator of cross-border transactions, to announce a new set of regulations on May 5, to be implemented in June.

The new regulations can be split into two parts, and broadly summarised as follows:

*a) The first measure targets Chinese bank balance sheets. This measure aims to:*

i) Directly reduce the scale of China’s FX loans, thus reducing the scale of letter of credit (LC) financing (bank loans), thereby reducing the volume of funding available for CCFDs (though not specifically targeting CCFDs); and/or

ii) Raise banks’ FX net open positions (banks are required to hold a minimum net long FX position at the expense of CNY liabilities), thus raising LC financing costs, thereby increasing the cost of funding CCFDs.

Specifically, Exhibit 2 shows that SAFE aims to implement a bank loan to bank deposit ratio of 75%-100% going forward, compared to an existing ratio of >150%.

*

*

*b) The second measure targets exporters and/or importers (‘trade firms’) by identifying any activities that mainly result in FX inflows above normal export/import backed activities (i.e. trades for the purpose of interest rate arbitrage, amongst others). This measure would force entities to curb their balance sheets if they are found to be involved in such activities.*

Since May10 SAFE has been requesting ‘trade firms’ provide detailed information of their balance sheets and trading records, in order to categorize them as either A-list or B-list firms by June 1, 2013. B-list firms will be required to reduce their balance sheet significantly by cutting any capital inflow related trade activities.

To avoid being categorized as a B-list firm by SAFE, ‘trade firms’ may reduce their USD LC liabilities in the near term, with CCFDs likely impacted. It is not yet clear what happens to the B-list firms once they are categorized as such. However, if B-list firms were prohibited from rolling their LC liabilities this could increase the pace of the CCFD unwind, since these trade firms would likely need to sell their liquid assets (copper included) to fund their LC liabilities accumulated through previous CCFDs.

These new regulations are likely to impact a number of markets and market participants. In this note we focus on the impact on CCFDs and the copper market. *Should a) and b) be enforced, copper financing deals are highly likely to be impacted.*

* * *

That explains China's macro thinking. But what does it mean for the actual Copper Financing Deal? The below should explain it:

*An example of a typical, simplified, CCFD*

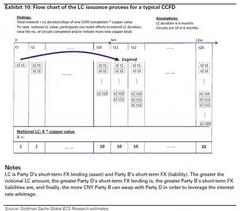

In this section we present an example of how a typical Chinese Copper Financing Deal (CCFD) works, and then discuss how the various parties involved are affected if the deals are forced to unwind. Exhibit 3 is a ‘simplified’ example of a CCFD, including specific reference to how the process places upward pressure on the RMB/USD. We believe this is the predominant structure of CCFDs, with other forms of Chinese copper financing deals much less profitable and likely only a small proportion of total deal volumes.

*A typical CCFD involves 4 parties and 4 steps:*

· *Party A *– Typically an offshore trading house

· *Party B –* Typically an onshore trading house, consumers

· *Party C *– Typically offshore subsidiary of B

· *Party D *– Onshore or offshore banks registered onshore serving B as a client

*Step 1) *offshore trader A sells warrant of bonded copper (copper in China’s bonded warehouse that is exempted from VAT payment before customs declaration) or inbound copper (i.e. copper on ship in transit to bonded) to onshore party B at price X (i.e. B imports copper from A), and A is paid USD LC, issued by onshore bank D*. The LC issuance is a key step that SAFE’s new policies target.*

*

*

*Step 2) *onshore entity B sells and re-exports the copper by sending the warrant documentation (not the physical copper which stays in bonded warehouse ‘offshore’) to the offshore subsidiary C (N.B. B owns C), and C pays B USD or CNH cash (CNH = offshore CNY). Using the cash from C, B gets bank D to convert the USD or CNH into onshore CNY, and trader B can then use CNY as it sees fit.* *

*The conversion of the USD or CNH into onshore CNY is another key step that SAFE’s new policies target*. This conversion was previously allowed by SAFE because it was expected that the re-export process was a trade-related activity through China’s current account. Now that it has become apparent that CCFDs and other similar deals do not involve actual shipments of physical material, SAFE appears to be moving to halt them.* *

*Step 3)* Offshore subsidiary C sells the warrant back to A (again, no move in physical copper which stays in bonded warehouse ‘offshore’), and A pays C USD or CNH cash with a price of X minus $10-20/t, i.e. a discount to the price sold by A to B in Step 1.* *

*Step 4)* Repeat Step 1-Step 3 as many times as possible, during the period of LC (usually 6 months, with range of 3-12 months). This could be 10-30 times over the course of the 6 month LC, with the limitation being the amount of time it takes to clear the paperwork. In this way, the total notional LCs issued over a particular tonne of bonded or inbound copper over the course of a year would be 10-30 times the value of the physical copper involved, depending on the LC duration.* *

*Copper ownership and hedging*: Through the whole process each tonne of copper involved in CCFDs is hedged by selling futures on LME futures curve (deals typically involve a long physical position and short futures position over the life of the CCFDs, unless the owner of the copper wants to speculate on the price).

Though typically owned and hedged by Party A, the hedger can be Party A, B, C and D, depending on the ownership of the copper warrant.

As Goldman further explains, the importance of CCFD is "*not trivial*" - that is an understatement: with the implicit near-infinite rehypothecation in which the number of "circuits" in the deal is only a factor of "the amount of time it takes to clear the paperwork", there may be hundreds of billions, if not more, in leverage resulting from this shadow transaction that has been used in China for years. *Now, that loop is about to end*. The reality is nobody can predict what the impact will be, but whatever it is - i) it will extract tremendous leverage from the system and ii) it will have adverse impacts on both China's ability to absorb inflation and grow its economy.

*How important are CCFDs? They are not trivial!*

Chinese ‘financing deals’, including CCFDs, are likely to contribute to China’s FX inflows since they involve direct FX inflows through China’s current account. Specifically, for CCFDs, the immediate cross-border conversion of FX to onshore CNY after Party C pays Party B for the copper warrant (Step 2) directly contributes to China’s FX inflows. In terms of outflows, the issuance of LC (FX short-term lending) by Party D to Party A (Step 1) is not associated FX outflow by definition, and when the LCs expire they tend to be rolled forward. Step 3 occurs offshore, so there is no inflow/outflow related to this transaction.

In this way, the net Chinese FX inflows/outflows associated with CCFDs are equivalent to the change in the value of the notional LCs. We make some broad estimates of how much of China’s short-term FX lending could be accounted for by CCFDs.

Specifically, our best estimate suggests that roughly 10% of China’s short-term FX lending could have been associated with CCFDs since the beginning of 2012 (Exhibit 4). In April 2013, we estimate that CCFDs accounted for $35-40 bn (stock) of China’s total short-term FX lending of $384 bn (stock), making various assumptions. More broadly, Chinese bonded inventories and short-term FX lending has been positively correlated in recent years (Exhibit 5).

Two key questions remain: how the upcoming unwind will impact each CCFD participant entity...

*How an unwind may impact each CCFD participant*

As we discussed on pages 4 and 5, SAFE’s new regulations target both banks’ LC issuance (first measure) and ‘trade firms’ trade activities (second measure). Here we discuss how the different entities (A, B, C, D) would likely adjust their portfolios to meet the new regulations (i.e. what happens in a complete unwind scenario).

*Party A: *Party A, without the prospect of $10-20/t profit per Step 1-3 iteration, *is likely to find it hard to justify having bonded copper sitting on its balance sheet* (the current LME contango is not sufficient to offset the rent and interest costs). As a result, *Party A’s physical bonded copper would likely become ‘available’, and Party A would likely unwind its LME short futures hedge.*

*Party B, C: *To avoid being categorized as a B-list firm by SAFE, Party B and C may reduce their USD LC liabilities by: 1) *selling liquid assets to fund the USD LC liabilities, and/or 2) borrowing USD offshore and rolling LC liabilities to offshore USD liabilities*. The broad impact of this is to reduce outstanding LCs, and CCFDs will likely be affected by this. It is not yet clear what happens to the B-list firms in detail once they are categorized as such. However, if B-list firms were prohibited from rolling their LC liabilities this would increase the pace of the CCFDs unwind. *In this scenario, these trade firms would have to sell their liquid assets (copper included) to fund their LC liabilities accumulated through previous CCFDs.*

*Party D: *To meet SAFE’s regulations, Party D will likely adjust their portfolios *by reducing LC issuance and/or increasing FX (mainly USD) net long positions*, which would directly reduce the total scale of CCFDs and/or raise the LC financing cost, respectively.

... And what happens to copper prices (hint: GTFO)

*Implications for copper - bonded copper moves from a positive carry asset to negative carry asset*

*Implications for copper - bonded copper moves from a positive carry asset to negative carry asset*

We expect that a complete unwind of CCFDs, everything else equal, is likely to be bearish for copper prices, LME spreads, and bonded premiums.

CCFDs involve a long copper physical positions and a short futures position on the LME. The physical position would be sold if CCFDs unwound and the short futures positions bought back. The newly available physical copper would not be financed by the China and ex-China interest rate differential anymore (not a positive carry asset anymore), and would instead need to be financed by a natural contango (in the interim copper becomes a negative carry asset), everything else equal.

Theoretically then, the physical market, over a short period (say, one quarter), may need to absorb as much as c.400kt of copper, equivalent to 8% of quarterly global copper supply.

By contrast, the LME futures market would need to absorb buying of c.0.2%-0.3% of quarterly traded LME volumes and c.6% of daily average 2012 open interest. The impact on the physical market is therefore likely to be relatively large, in spite the fact that an unwind of CCFDs does not result in the creation of new copper (i.e. aggregate global copper inventory impact is 0/our inventory chart does not change).

*What about in practice?*

Since there are no comparable historical examples to make reference to, what happens when CCFDs unwind in practice is open for debate. We believe that since the downward pressure on the physical market is large, both in absolute terms and relative to the upward pressure on the futures market, near-term prices are likely to come under relatively significant pressure. Further, if the market fears the unwind of CCFDs, physical buyers may hold off on purchases, and futures sellers may bet on lower prices (offsetting either in part or more than offsetting the financing deal related unwind buying). In this way it is likely that in practice the whole copper price curve would be under pressure in the case of a complete CCFD unwind, at least until the contango widens sufficiently to compensate for the cost of carry.

We see the following as a likely chain of events in a complete unwind scenario:

· *China would draw on bonded until it is ‘full’. *In the current market bonded copper stocks will likely initially flow into the domestic Chinese market, since SHFE prices are above LME prices, with the SHFE curve in backwardation and LME in contango.

· *Chinese imports fall/remain low, placing upward pressure on LME stocks*. Since China is drawing bonded inventories to meet its demand, Chinese copper imports are likely to be under downward pressure beyond May, resulting in any excess material ex-China turning up on the LME as well (Exhibit 7). *Remaining bonded stocks (ex-stocks in transit), would shift to LME*. Once China is ‘full’ (i.e. the import arbitrage closes, bonded physical premia decline, SHFE price and curve softens), the remaining excess bonded inventory will likely make its way on to the LME. Since China is in deficit at present (drawing bonded and SHFE inventories, SHFE in backwardation), due in part to seasonal factors, the inventory numbers noted above, in practice, will likely be smaller but still very large. *Our best estimate would be a minimum of 200,000-250,000t of stock could shift/build on the LME over the next 2-3 months, or 4%-5% of quarterly global consumption. *

· *LME contango to widen. *Higher LME stocks suggest higher LME copper spreads, including downward pressure on the front end. Exhibit 8 illustrates that over the last 6 years, the buildup of LME inventory has been consistently associated with widening LME spreads into contango, and the scale of contango is mostly driven by financing cost and inventory levels. With excess copper flowing into LME warehouses, the spread needs to widen further to finance the carry trade effectively. For reference, LME annual rents are c.$150/t or 2% of copper prices. Assuming an annualized financing cost of 1%-1.5%, full carry is c.3%-3.5%, compared to current LME 3-15 month contango of 1.1%.

The main caveat to the above is that a complete unwind in CCFDs is still subject to the implementation of the policy by SAFE, Chinese banks and ‘trade firms’, and the possibility that new financing deals are “invented”. As a result, we will continue to closely monitor implementation of the policy by banks via monitoring bonded physical premiums, SHFE spreads and bonded stock flows.

Finally, what does all this mean for explicit rehypothecation chain leverage (initially just at the CCFD level although a comparable analysis must be done for systemic as well) and CCFD risk exposure:

*Leverage in CCFDs*

Below is a demonstration of the LC issuance process in a typical CCFD. Assuming an LC with a duration of 6 months, and 10 circuit completions (of Step 1-3) during that time (i.e. one CCFD takes 18 days to complete), Party D is able to issue 10 times the copper value equivalent in the form of LCs during the first 6 month LC (as shown from period t1 to t10 in Exhibit 10). In the proceeding 6 months (and beyond), the total notional value of the LCs remains the same, everything else equal, since each new LC issued is offset by the expiration of an old one (as shown from period t11 to t20).

*In this example, total notional amount of LC during the life of the LC = LC duration / days of one CCFD completion* copper value = 10. In this example, the total notional amount of LC issued by Party D, total FX inflow through Party D from party A, and total CNY assets accumulated by party B (and C) are all 10 times the copper value (per tonne).*

To raise the total notional value of LCs, participants could:

· Extend the LC duration (for example, if LC duration in our model is 12 months, the notional LC could be 20 times copper value)

· Raise the no. of circuits by reducing the amount of time it takes to clear the paperwork

· Lock in more copper

*Risk exposures of parties to CCFDs*

Theoretically, Party B risk exposure > Party D risk exposure > Party A risk exposure

· Party B’s risks are duration mismatch (LC against CNY assets) and credit default of their CNY assets;

· Party D’s risks are the possibility that party B has severe financial difficulties. (they manage this risk by controlling the total CNY and FX credit quota to individual party B based on party B’s historical revenue, hard assets, margin and government guarantee) (Party D has the right to claim against party B (onshore entity), because party B owes party D short term FX debt (LC)). If party B were to have financial difficulties, party D can liquidate Party B’s assets.

· Party A’s risk is mainly that party D (China’s banks) have severe financial difficulties (Party A has the right to claim against party D (onshore banks), because Party A (or Party A’s offshore banks) holds an LC issued by party D). In the case of financial difficulties for Party B, and even in case Party D has difficulties, Party A can still get theoretically get paid by party D (assuming Party D can borrow money from China’s PBoC).

In brief (pun intended): a complete, unpredictable clusterfuck accompanied by wholesale liquidations of "liquid assets", deleveraging and potentially a waterfall effect that finally bursts China's bubble, all due to a simple black swan. Although, in reality, nobody knows. Just like nobody knew what would happen when the government decided to let Lehman fail.

So... is this China's Lehman? Reported by Zero Hedge 10 hours ago.

↧

↧

Analyst Jeff Kagan on Softbank Trying to Ease China Concerns over Sprint Merger

Softbank approval is more difficult due to Chinese security concerns. Technology Industry Analyst Jeff Kagan is available to speak with reporters, or may be quoted through this release.

Atlanta, GA (PRWEB) May 23, 2013

Softbank is trying to acquire Sprint Nextel. Softbank is a Japanese company. US regulators are worried about any Softbank security concerns with China. Softbank is trying to make this deal acceptable to US regulators, so says this CNET piece from May 22, 2013.

Tech analyst Jeff Kagan offers comment on this story.

“This proposed Softbank deal to acquire Sprint Nextel seemed to make sense since it started several months ago. However we all knew approval would be more difficult than normal because of the China security threat. Softbank CEO Masayoshi Son has been working hard, trying to clear the path for this deal to be approved.” Says Wireless analyst Jeff Kagan.

Softbank CEO Masayoshi Son previously said he would remove Huawei equipment, which the US had a problem with. Now he says one of the directors could be from the US Government, keeping their eye on security.

“Masayoshi Son is doing the right thing and trying to remove US concerns in order to get this deal approved. The question is, will it be enough? Will this deal be approved?” Asks telecom analyst Jeff Kagan.

“Sprint is in a great place right now. Sprint is wanted by more than one company. That means they get to choose. Both Softbank and DISH Network want Sprint and Clearwire. Only one will win. Which one is the question? They both have strengths and weaknesses. So the question is which will Sprint choose? No one knows yet, but either way, the Sprint of tomorrow will look very different from the Sprint of today.” Says Kagan.

About Jeff Kagan

Jeff Kagan is a Technology Industry Analyst who is regularly quoted by the media over 25 years. He offers comment on wireless, telecom and tech news stories to reporters and journalists.

He is also known as a Tech Analyst, Wireless Analyst, Telecom Analyst and Principal Analyst depending on the focus of the story.

He follows wireless, telecom, Internet, cable television and IPTV. He also follows the wide consumer electronics and technology space.

Reporters: Jeff Kagan sends comments by email to reporters and the media. If you would like to be added to this email list please send request by email.

Clients: Call or email Jeff Kagan to discuss becoming a client. Kagan has worked with many companies over 25 years as consulting clients.

Contact: Jeff Kagan by email at jeff(at)jeffKAGAN(dot)com or by phone at 770-579-5810.

Visit his website: at jeffKAGAN.com to learn more and for disclosures.

Kagan is an analyst, consultant, columnist and speaker.

Twitter: @jeffkagan Reported by PRWeb 10 hours ago.

Atlanta, GA (PRWEB) May 23, 2013

Softbank is trying to acquire Sprint Nextel. Softbank is a Japanese company. US regulators are worried about any Softbank security concerns with China. Softbank is trying to make this deal acceptable to US regulators, so says this CNET piece from May 22, 2013.

Tech analyst Jeff Kagan offers comment on this story.

“This proposed Softbank deal to acquire Sprint Nextel seemed to make sense since it started several months ago. However we all knew approval would be more difficult than normal because of the China security threat. Softbank CEO Masayoshi Son has been working hard, trying to clear the path for this deal to be approved.” Says Wireless analyst Jeff Kagan.

Softbank CEO Masayoshi Son previously said he would remove Huawei equipment, which the US had a problem with. Now he says one of the directors could be from the US Government, keeping their eye on security.

“Masayoshi Son is doing the right thing and trying to remove US concerns in order to get this deal approved. The question is, will it be enough? Will this deal be approved?” Asks telecom analyst Jeff Kagan.

“Sprint is in a great place right now. Sprint is wanted by more than one company. That means they get to choose. Both Softbank and DISH Network want Sprint and Clearwire. Only one will win. Which one is the question? They both have strengths and weaknesses. So the question is which will Sprint choose? No one knows yet, but either way, the Sprint of tomorrow will look very different from the Sprint of today.” Says Kagan.

About Jeff Kagan

Jeff Kagan is a Technology Industry Analyst who is regularly quoted by the media over 25 years. He offers comment on wireless, telecom and tech news stories to reporters and journalists.

He is also known as a Tech Analyst, Wireless Analyst, Telecom Analyst and Principal Analyst depending on the focus of the story.

He follows wireless, telecom, Internet, cable television and IPTV. He also follows the wide consumer electronics and technology space.

Reporters: Jeff Kagan sends comments by email to reporters and the media. If you would like to be added to this email list please send request by email.

Clients: Call or email Jeff Kagan to discuss becoming a client. Kagan has worked with many companies over 25 years as consulting clients.

Contact: Jeff Kagan by email at jeff(at)jeffKAGAN(dot)com or by phone at 770-579-5810.

Visit his website: at jeffKAGAN.com to learn more and for disclosures.

Kagan is an analyst, consultant, columnist and speaker.

Twitter: @jeffkagan Reported by PRWeb 10 hours ago.

↧

MDC Partners Expands Global Footprint with China Offerings

NEW YORK, May 23, 2013 /PRNewswire/ --MDC Partners announced today that partner agency Anomaly is opening a Shanghai office, further extending MDC's global footprint in China. The Anomaly China of...

Reported by FinanzNachrichten.de 9 hours ago.

↧

BLANKFEIN: Don't Worry, Goldman Isn't Giving Up On China Yet

Last night's bad PMI number seems to have been the tipping point in a recent build up of bad Chinese data that came in last month. This morning, the Nikkei fell by 7.3%, and markets around Europe are down as well.

News from Goldman Sachs earlier this week probably didn't help either. The bank exited the massive investment it made in the Industrial and Commercial Bank of China back in 2006. It was made even before ICBC became the 2nd biggest IPO in history. The stock, though volatile to say the least, is up 57.1% since that year.

So, even though Goldman has sold off pieces of its stake in ICBC five times since it 2010, with all this bad news coming out about China, it's hard not to ask — why now? Does Goldman buy the China bear argument that the increasing cost of credit in the country will cripple growth?

Goldman Sachs CEO Lloyd Blankfein was on Bloomberg TV this morning giving a firm answer amidst all the chaos.

Here's what he told anchor Erik Schatzker:

"Well, first of all, catch the wave when it comes-- I don't know if you've been watching but there has been a wave and it's been going on for quite some time. It may be interrupted. ICBC, again, is not the key to our interest in China or the big reflection of it.* ICBC was an investment we made at a time when China was taking its banking system public and was looking for partners-- really, kind of quasi-strategic partner-- to help-- not only provide investment capital but also expertise. And so they wanted firms like ourselves. * And there were other financial institutions that partnered with other banks. And so we ended up holding that investment for a while. But through that investment we became very close with important people in the banking system. And we maintain that relationship today. We're investing in China because China-- I was going to say it's the future-- but it's a big part of the present as well."

Blankfein went on to say that Goldman would be happy to make an ICBC sized investment again, but the time would have to be right.

Does that calm anyone's nerves?

Watch the full interview below:

Please follow Clusterstock on Twitter and Facebook.

Join the conversation about this story »

Reported by Business Insider 8 hours ago.

News from Goldman Sachs earlier this week probably didn't help either. The bank exited the massive investment it made in the Industrial and Commercial Bank of China back in 2006. It was made even before ICBC became the 2nd biggest IPO in history. The stock, though volatile to say the least, is up 57.1% since that year.

So, even though Goldman has sold off pieces of its stake in ICBC five times since it 2010, with all this bad news coming out about China, it's hard not to ask — why now? Does Goldman buy the China bear argument that the increasing cost of credit in the country will cripple growth?

Goldman Sachs CEO Lloyd Blankfein was on Bloomberg TV this morning giving a firm answer amidst all the chaos.

Here's what he told anchor Erik Schatzker:

"Well, first of all, catch the wave when it comes-- I don't know if you've been watching but there has been a wave and it's been going on for quite some time. It may be interrupted. ICBC, again, is not the key to our interest in China or the big reflection of it.* ICBC was an investment we made at a time when China was taking its banking system public and was looking for partners-- really, kind of quasi-strategic partner-- to help-- not only provide investment capital but also expertise. And so they wanted firms like ourselves. * And there were other financial institutions that partnered with other banks. And so we ended up holding that investment for a while. But through that investment we became very close with important people in the banking system. And we maintain that relationship today. We're investing in China because China-- I was going to say it's the future-- but it's a big part of the present as well."

Blankfein went on to say that Goldman would be happy to make an ICBC sized investment again, but the time would have to be right.

Does that calm anyone's nerves?

Watch the full interview below:

Please follow Clusterstock on Twitter and Facebook.

Join the conversation about this story »

Reported by Business Insider 8 hours ago.

↧

FIDELITY CHINA SPECIAL SITUATIONS PLC - Total Voting Rights

Fidelity China Special Situations PLC Voting Rights and Capital as at 23 May 2013. This announcement is made in accordance with DTR5.6.1. As at 23 May 2013 Fidelity China Special Situations PLC's ...

Reported by FinanzNachrichten.de 8 hours ago.

↧

↧

North Korea ready to accept China's peace effort

A special North Korean envoy said in Beijing yesterday that Pyongyang would accept China's suggestion that it restart talks with relevant parties to restore a peaceful environment on the Korean peninsula, China Central Television said last night.

Reported by S.China Morning Post 3 hours ago.

↧

China set to send troops to Mali

China has offered to send more than 500 soldiers to the UN force seeking to contain Islamist militants in Mali in what would be its biggest contribution to UN peacekeeping, diplomats said in New York.

The move could be a bid to overcome tensions with the West over the Syria conflict and to strengthen China's relations in Africa, where it is a major buyer of oil and other resources, diplomats and experts said. Reported by S.China Morning Post 3 hours ago.

The move could be a bid to overcome tensions with the West over the Syria conflict and to strengthen China's relations in Africa, where it is a major buyer of oil and other resources, diplomats and experts said. Reported by S.China Morning Post 3 hours ago.

↧

China takes battering in poll of perceptions in 25 nations and EU

Global views of China's influence have deteriorated sharply, according to a poll conducted for the BBC's World Service, reaching their lowest level in years.

Analysts said the change reflected China's increasing positive and negative involvement in international affairs. Reported by S.China Morning Post 3 hours ago.

Analysts said the change reflected China's increasing positive and negative involvement in international affairs. Reported by S.China Morning Post 3 hours ago.

↧